{kind=link}

On the back of the Covid-19 pandemic, sovereign risk has increased in several countries across the globe. For countries experiencing a debt crisis, the restructuring of government bonds is a possible resolution tool. Whether investors perceive restructuring to be in their interest can be crucial for successful debt operations. While much of the literature researching financial implications of debt restructuring has focused on investors’ short-term losses, we provide evidence on investment returns over the longer run (Andritzky and Schumacher 2019). Surprisingly, we find that bond returns over the longer run – capturing both pre- and post-crisis times – do not differ significantly between crises with and without a debt restructuring. What matters much more is bondholders’ investment strategy during crises episodes: conditional on a debt crisis, debt restructuring can even be financially rewarding for creditors investing in distressed bonds.

Empirical evidence shows that resolving a debt crisis through a restructuring of government debt can reduce the economic costs for the debtor country (Asonuma et al. 2019). Creditors, however, are often perceived to suffer sizable losses under such circumstances: Cruces and Trebesch (2013) find that investors participating in bond exchanges since the 1970s incurred present value losses (or ‘haircuts’) of 40% on average. Taking an even longer view, Meyer et al. (2019) show that losses of similar size have been the norm since the early 19th century.

In a recent paper (Andritzky and Schumacher 2019), we look at long-term returns with a different perspective, studying investors’ wins or losses depending on how a crisis is resolved. Whereas a ‘haircut’ captures the loss (typically computed in net present value terms) at a single point in time, creditors usually take a longer-term perspective. The total return on their investment is also determined by earnings prior to a debt exchange, such as from often substantial coupons and the potential recovery in the bonds’ market value after a crisis is resolved.

This suggests that debt restructuring can be more than a zero-sum wealth transfer from creditors to debtors. By improving debt sustainability, restructuring can bolster confidence and reduce debt overhang, in turn supporting economic recovery and post-crisis expansion (e.g. Reinhart and Rogoff 2010). Thus, a restructuring that facilitates a transition from a crisis equilibrium with high yields and depressed bond prices to a non-crisis equilibrium of low-risk spreads and restored market access may offer upsides not only to debtors, but also to creditors, at least in the longer run.

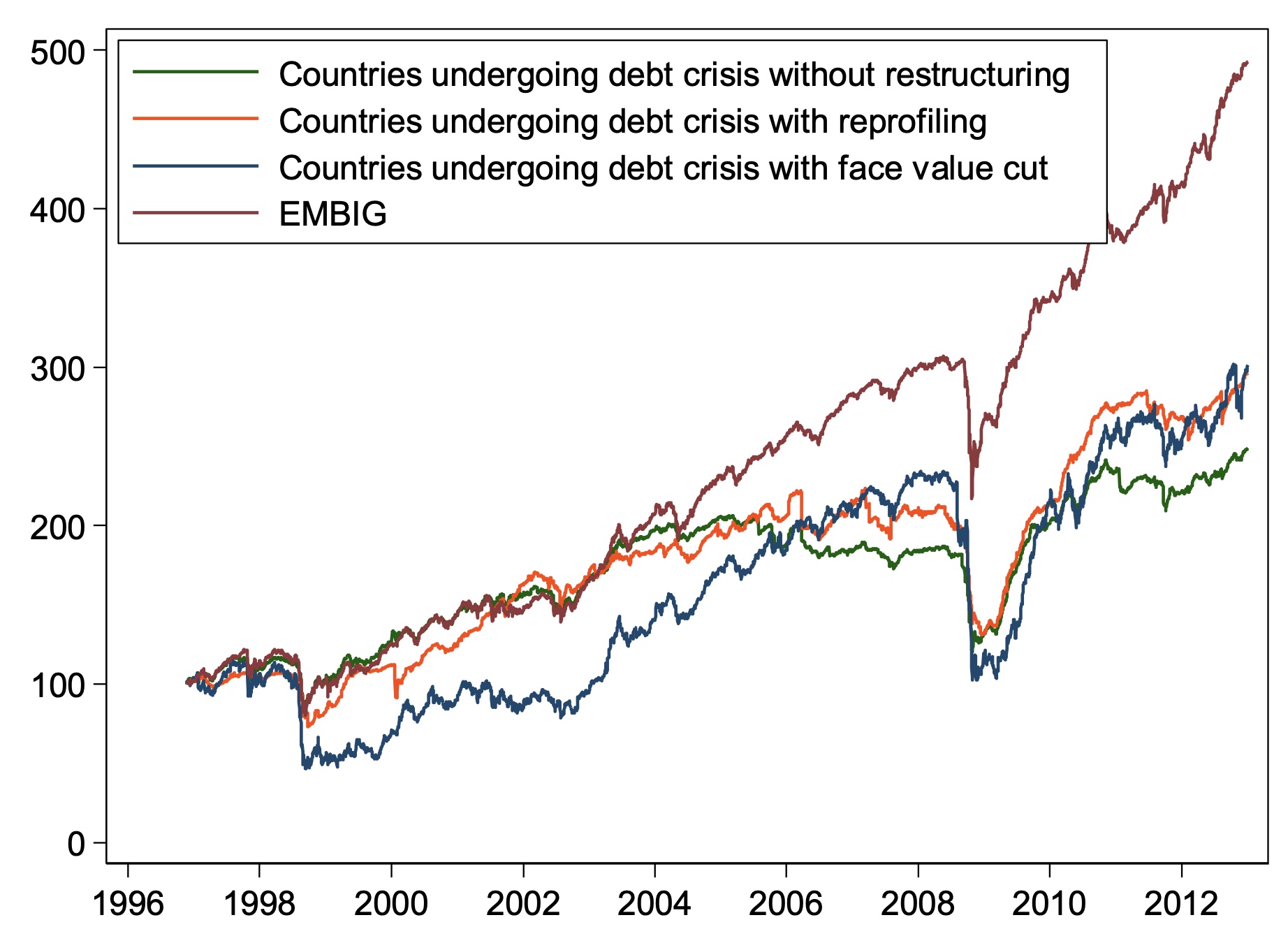

Crisis, not crisis resolution, matters

In our analysis, we compute long-term returns of sovereign bonds issued by countries during 32 emerging market crisis episodes at the individual instrument level. We thereby take the performance of all assets received in debt exchanges, including new bonds, cash transfers or warrants into account. Besides gross returns, we calculate excess returns vis-à-vis US Treasuries as well as the risk-adjusted returns (Sharpe ratio). In order to identify debt crises, we deploy a range of different definitions, including a market-based measure (sovereign spreads exceeding 1000 basis points) and a ratings-based measures (sovereign ratings falling below B or equivalent) and cross-check these result against other indicators such as IMF-supported programs. We then distinguish crises that were resolved without any restructuring of debts from crises in which the terms and conditions of the bonds were adjusted. We further divide the latter cases into cases where restructurings mainly consisted of maturity extensions (‘reprofiling’) and cases where restructuring was aimed at debt reductions (‘face value cut’).

Our results suggest that bonds issued by countries experiencing a sovereign debt crisis have indeed yielded lower returns than a broader market index of emerging market government bonds (Figure 1). Conditional on experiencing a debt crisis, however, the modalities of crisis resolution – whether or not debt is restructured, and how – does not have a significant impact on creditors’ returns. Indeed, over a window of about 15 years, a bond portfolio of crisis countries undergoing restructurings yielded a slightly higher total gross return than a portfolio of crisis countries without. Both portfolios roughly doubled in value.

Figure 1 Cumulative returns by crisis resolution type

Source: Andritzky and Schumacher (2019).

Importantly, we find that some investment strategies would have returned significantly higher returns ex post than others. Comparing the returns of ‘constrained’ investors selling their holdings at the start of a crisis to ‘distress’ investors entering the market at the same time, suggests that constrained investors generally fare worse, mostly because they are unable to avoid part of the pre-crisis decline in prices but miss most of the recovery rally (Figure 2). Distressed debt investors, in contrast, may reap very considerably upsides.

Even in risk-adjusted terms, distress investors may fare better than constrained investors. The latter may include institutional investors who are often obliged to follow a constrained investment strategy. Taking together all crisis episodes, a constrained investor type would have realised an average annualized excess return of -1.8% at a Sharpe ratio of -0.1. In contrast, the distress investor would have been able to reap an average annualized excess return of 17.2% at a Sharpe ratio of 0.9, on both metrics also beating a passive buy-to-hold strategy throughout the entire crisis episode.

Figure 2 Excess returns for constrained and distress investors during crisis episodes

Source: Andritzky and Schumacher (2019).

No act of charity

Our findings underpin the idea that debt restructuring can be more than a zero-sum wealth transfer from creditors to debtors. The insight that buy-and-hold investors would have been able to realize high (risk-adjusted) ex-post returns even in crises that are resolved by a debt operation is a key lesson for the current policy debate on resolving debt crises. Such excess returns could be interpreted as a premium compensating for the risks associated with a debt operation, such as holdout investors trying to thwart a debt exchange. The uncertainties surrounding debt operations may contribute to the slump in bond prices typically observed during crises, which are possibly reinforced by rigid investment mandates or regulatory requirements. Hence, improvements to the debt restructuring process, for instance through clear procedures or strengthened collective action clauses, may reduce uncertainty and risk premia. This may render debt restructuring more credible and effective as a crisis resolution tool.

Authors’ note: The views expressed herein are those of the authors and should not be attributed to the ECB or the IMF, its Executive Board, or its management or policies.

References

Andritzky, J and J Schumacher (2019), “Long-Term Returns in Distressed Sovereign Bond Markets: How Did Investors Fare?” IMF Working Paper No. 19/138.

Asonuma, T, M Chamon, A Erce and A Sasahara (2019), “Costs of Sovereign Defaults: Restructuring Strategies, Bank Distress and the Capital Inflow-Credit Channel,” IMF Working Paper No. 19/69.

Cruces, J J and C Trebesch (2013), “Sovereign Defaults: The Price of Haircuts”, American Economic Journal: Macroeconomics 5(3): 85–117.

Krugman, P (1988), “Financing vs. Forgiving a Debt Overhang”, Journal of Development Economics 29: 253-268.

Meyer, J, C Reinhart and C Trebesch (2019), “Sovereign Bonds since Waterloo”, NBER Working Paper No. 25543.

Reinhart, C M and K S Rogoff (2010), “Debt and Growth Revisited,” VoxEU.org, 11 August.